The price mechanism

In a market economy resources are allocated primarily through the price mechanism. Prices act as signals and incentives: when demand for a good increases, its price tends to rise. The higher price encourages producers to increase output and attracts resources into that industry. Conversely, a fall in price discourages production and resources are freed for other uses. Through this process of supply and demand, markets coordinate the decisions of millions of buyers and sellers without central direction.

Functions of price

Prices perform three key functions:

- Signalling – prices provide information about market conditions. A high price signals scarcity whereas a low price indicates abundance.

- Incentive – price changes create incentives for producers and consumers to change their behaviour. Rising prices encourage production while falling prices encourage consumption.

- Rationing – scarce resources must be rationed among competing uses. Prices help determine who obtains goods and services based on willingness and ability to pay.

| Scenario | Price response | Resource allocation |

|---|---|---|

| Increase in demand for electric cars | Price of electric cars rises | Manufacturers invest in battery and car production; resources shift towards electric vehicle industry |

| Discovery of new oil reserves (increase in supply) | Price of oil falls | Oil production becomes less profitable; resources move to other sectors |

| Government imposes tax on sugary drinks | Price of sugary drinks rises | Consumers switch to healthier alternatives; producers may reformulate products |

Although markets can allocate resources efficiently, there are situations where the price mechanism fails to achieve the best outcome (see Chapter 14 on market failure). Government intervention may then be needed through taxes, subsidies or regulation.

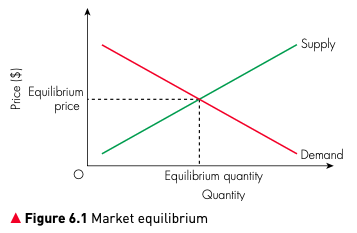

Market equilibrium and disequilibrium

The market system is the method of allocating scarce resources through the forces of demand and supply. In a competitive market, an equilibrium price emerges where the quantity demanded equals the quantity supplied. At this price and quantity combination, all products offered for sale are bought and there are no shortages or surpluses.

If the market price is set above the equilibrium price, the quantity supplied exceeds the quantity demanded, creating a surplus. Producers will lower prices to clear this excess supply. Conversely, if the price is below equilibrium, demand exceeds supply, leading to a shortage; prices then rise to encourage more supply. This process of price adjustment eliminates market disequilibrium, which occurs when the price is too high (resulting in excess supply) or too low (resulting in excess demand).

Key economic questions

Every economic system must address three fundamental questions about resource allocation:

- What to produce? Decision makers must determine which goods and services should be provided. Because resources are limited, producing more of one thing means sacrificing production of another, so opportunity cost must be considered.

- How to produce? This concerns the methods and processes used to make goods and services. It involves deciding the combination of factors of production — land, labour, capital and enterprise — to use.

- For whom to produce? This question addresses which groups receive goods and services. It considers whether products should be provided free to everyone or only to those willing and able to pay.